Financial planning experts have outlined a series of steps for individuals to create effective personal budgets, emphasizing the importance of managing money regardless of income level. They note that without a plan, overspending, debt struggles, and unmet financial goals are common outcomes.

A budget is described as a written plan mapping out monthly spending based on anticipated income, expenses, and savings goals. Experts state that managing money with a budget ensures earned income is used according to personal goals and values, while lack of one can lead to running out of funds before paychecks, debt issues, poor credit, and other negative consequences.

The process begins with establishing financial goals, both short-term and long-term. Long-term goals like funding retirement or education may take decades, while short-term goals such as building an emergency fund, paying down debt, or saving for vacations can provide motivation. Experts advise making a list of these goals to clarify objectives.

Calculating net income, or take-home pay after taxes and deductions, is highlighted as a critical step to determine available money for spending and saving each month. Experts recommend understanding this figure before proceeding.

Multiple budgeting methods are available, and individuals are encouraged to try different types to find a suitable fit. Popular options include the 50/30/20 rule, which allocates 50% to needs, 30% to wants, and 20% to savings and debt; the 80/20 rule with 20% for savings and investments; zero-based budgeting assigning every dollar a job; envelope budgeting using physical or digital cash; reverse budgeting prioritizing savings; spreadsheet budgets for customization; and values-based budgets tied to personal values.

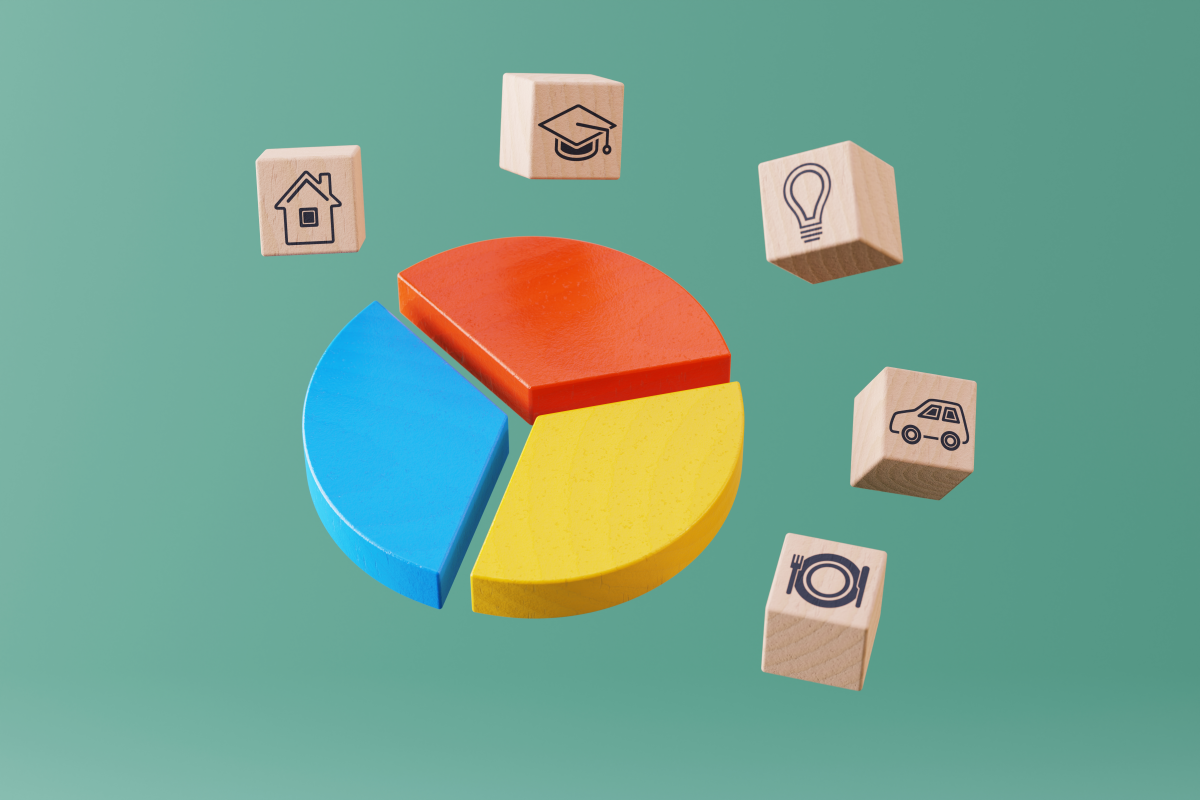

Including monthly expenses is the next step, with experts suggesting reviewing credit card and bank statements to understand past spending. Common budget categories listed are bills (rent, utilities, insurance), debt payments (loans, credit cards), essential needs (groceries, gas, healthcare), discretionary spending (dining, entertainment), and savings (emergency fund, retirement). They differentiate between fixed expenses, which remain consistent like car payments, and variable expenses, which fluctuate like groceries and gas, noting that variable expenses are easier to adjust for savings.

After creating a budget, experts recommend a trial run and regular reviews to make adjustments, especially if expenses exceed income. They note that fine-tuning is normal and part of the process.

Tips for sticking to a budget include using apps or software to track expenses, reducing spending to free up cash, and consulting financial professionals like coaches or credit counselors for guidance. Experts highlight benefits such as correcting poor spending habits, paying down and avoiding new debt, and reducing financial stress.

In summary, experts assert that budgets are powerful tools for reaching financial goals, and there is no perfect method for every situation. They encourage trying multiple strategies and making adjustments until finding a solution that works, emphasizing that trial and error is beneficial and changes indicate active money management.